Maximieren Sie Ihren Verkaufserfolg!

Die Vendor Due Diligence (VDD) ist entscheidend im Unternehmensverkauf und bietet Verkäufern einen strategischen Vorteil. Durch unabhängige Dritte erfolgt eine objektive Bewertung und Analyse des Unternehmens, um Chancen und Risiken zu identifizieren. VDD geht über traditionelle Due Diligence Prüfungen hinaus und gewährleistet Transparenz. Diese proaktive Herangehensweise verbessert die Kommunikation und beschleunigt den Verkaufsprozess.

Im Gegensatz zur Buy Side Due Diligence, die die Sorgfalt des Käufers betont, unterstreicht die VDD die Interessen des Verkäufers. Diese Vorgehensweise optimiert M&A Transaktionen und erhöht die Wahrscheinlichkeit eines erfolgreichen Abschlusses.

Nachfolgend werden wir die grundlegenden Prinzipien der Vendor Due Diligence, ihren Umfang und die spezifischen Inhalte, die in Betracht gezogen werden sollten, näher betrachten. Außerdem erfahren Sie, wann eine VDD sinnvoll ist und welche Vorteile sie konkret bietet.

Die Vendor Due Diligence im Kurzüberblick:

- Basic principle: Vendor due diligence is a decisive step in the process of Company sale, initiated by the sellerto enable a transparent and objective evaluation of the company prior to acquisition.

- Flexibility in scopeThe The level of detail of the VDD is customisable and is determined by the seller according to the needs and strategic objectives of the company acquisition. This enables a customised presentation of the company.

- Purpose and benefitsThe aim of the VDD is to provide a comprehensive and in-depth insight into the company in order to the sales position to strengthen and Potential risks for the acquisition at minimise. Ergänzend hierzu liefert die Commercial Due Diligence wertvolle Informationen über Marktbedingungen und Wettbewerbsumfeld.

- AddresseesThe results of the VDD are provided specifically to potential buyers or as part of auction proceduresto speed up the acquisition process and support the decision-making process of interested parties.

Table of contents

- Maximieren Sie Ihren Verkaufserfolg!

- Die Vendor Due Diligence im Kurzüberblick:

- What is Vendor Due Diligence?

- Vorteile der Vendor Due Diligence

- Vendor Due Diligence Inhalte: Finanzielle, Steuerliche und Rechtliche Aspekte

- Erstellung und Verantwortlichkeiten der Vendor Dud Diligence

- When does VDD make sense for sellers?

- Conclusion

What is Vendor Due Diligence?

A vendor due diligence is a company audit that is carried out for a company for sale by the seller. before the Company sale is carried out.

The audit is carried out by the seller’s appointed advisors, who should, however, be independent. The extent to which the VDD is carried out and the exact areas of the company to be audited are left to the seller’s discretion. As a rule, a “neutral” audit is certified.

Durch die Vendor Due Diligence sollen die Strengths and weaknesses of the company revealed be made. This gives the seller the opportunity to compensate for possible weaknesses in advance, if necessary, and the buyer quickly gets a good overview of the company. The VDD is also well suited for a parallel bidding process.

Vorteile der Vendor Due Diligence

- Through the Due Diligence Report, the seller can Identify weak points in his company and eliminate thembefore the buyer undertakes a possible extended inspection.

- The effort for the buyer side is reduced and thus the process of selling the company can be facilitated and accelerated.

- By identifying weak points or grievances early on, the seller can Go into sales negotiations better prepared and argue better accordingly.

- The chance of finding a buyer more quickly is higher, as the buyer has the opportunity to get a good overview of the company for sale at an early stage and this provides him with a corresponding degree of security without having to trigger an extensive DD process himself immediately.

- The Transaction process of the sale is acceleratedas the buyer does not have to carry out an inspection to this extent by the VDD itself; this saves time.

Learn in our webinar which further measures are crucial for an effective business sale:

In our online seminar Selling a Business you will learn how to find the right buyer for your company.

Vendor Due Diligence Inhalte: Finanzielle, Steuerliche und Rechtliche Aspekte

Vendor due diligence is often prepared according to the thematic areas of a company.

Da zum Zeitpunkt der Beauftragung des Vendor Due Diligence Reports die möglichen Kaufinteressenten und deren spezifischer Fokus noch nicht bekannt ist, besteht die Vendor Due Diligence häufig aus der Financial, Tax and Legal Due Diligence. Supplemented, if necessary, by Market and Environmental (environmental risks).

Since the project commissioned by the buyer Due Diligence and the VDD are similar in their basic structure, we would like to present our Due Diligence Checklist:

Highlight your company’s strengths with due diligence and justify the purchase price you are seeking. Check the most important points now.

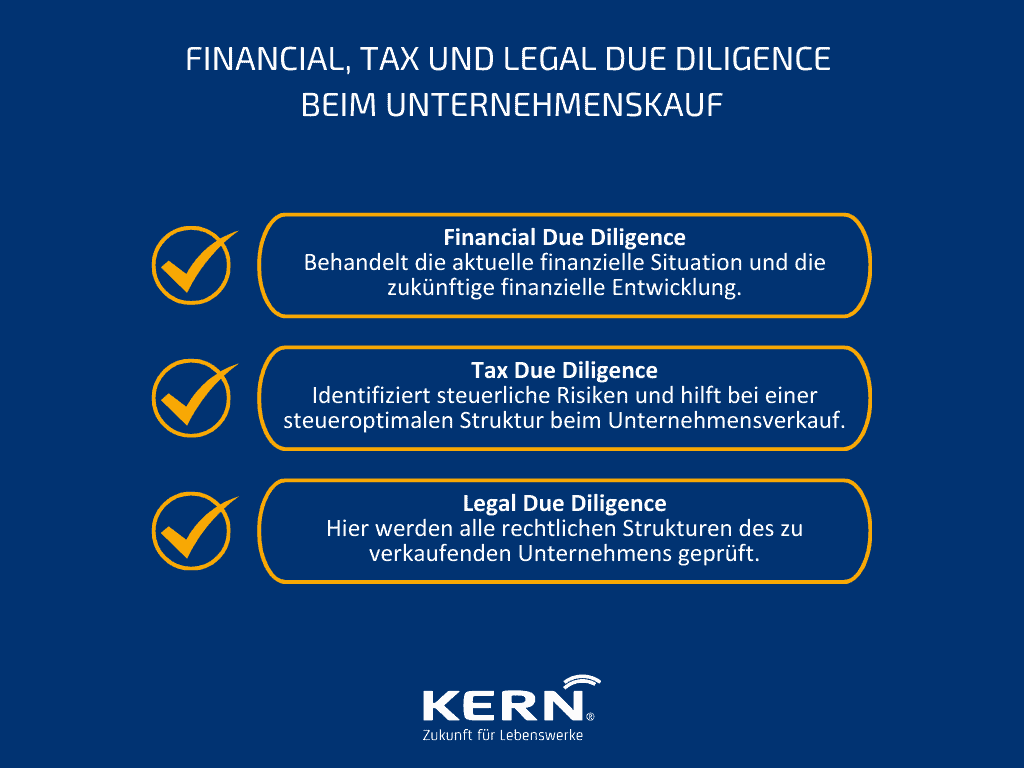

Financial Due Diligence

Financial due diligence deals in detail with the finances of the company. This involves both the Current financial situation as well as future financial development.

Tax Due Diligence

Tax due diligence presents the tax situation of the company, identifies tax risks and thus helps to create a tax-optimised structure for the sale of a company. and to limit risks in the future after the sale.

Legal Due Diligence

During legal due diligence, all legal structures of the company to be sold are examined. The subject of the legal due diligence is above all Shareholders’ agreement, ownership and contracts with staff and suppliers.

Umfang der Vendor Due Diligence

The VDD can be carried out in different ways. The seller can have a detailed report prepared on the individual areas or only a descriptive fact bookwhat is to be presented to the prospective buyers.

The Fact Book will then be made available to potential buyers. Together with the Non-Reliance Letter handed out.

Fact Book

Der Bericht der Vendor Due Diligence wird häufig als Fact Book bezeichnet. Das ist meist nur ein deskriptiver Bericht der VDD. Dieses Fact Book wird den Kaufinteressenten zu Beginn der Verhandlungen vorgelegt. Das Fact Book provides a transparent and well-founded overview of the company for sale.

In addition, there is the advantage here that not all of the company’s sensitive data has to be disclosed. Through the Descriptive design of the Fact Book the buyer receives a Sound and transparent overview of the companybut not sensitive details.

Especially if the company is to be sold in an auction process, the Fact Book from the VDD is indispensable and has now become standard.

Non-Reliance Letter

A Non-Reliance Letter is the English term for a contractual disclaimer.

The Non-Reliance Letter is handed out to bidders in an auction procedure with the Fact Book and must be signed by them.

The Non-Reliance Letter includes a Bidders’ reliance on the accuracy and completeness of the VDD reportof the Fact Book.

Erstellung und Verantwortlichkeiten der Vendor Dud Diligence

Vendor due diligence is generally carried out before the sale of a company. As a rule, it is already carried out when the sale of the company is planned but there are no prospective buyers yet.

In order to get as realistic a picture of the company as possible and to gain the trust of potential buyers, the Vendor due diligence by an independent third party, a lawyer, auditor or tax advisor carried out.

The report that is then prepared is issued to the potential buyers as a so-called Fact Book. In addition, the prospective buyers receive the Non-Reliance Letter.

As experienced advisors in matters of Company sale we will be happy to assist you with our expertise.

When does VDD make sense for sellers?

Vendor due diligence can be useful for the seller for several reasons. VDD is particularly useful if, for example, the seller wants to provide identical framework conditions in a bidding process and wants to increase the pace by providing comprehensive data.

Durch das frühzeitige Erstellen einer Vendor Due Diligence hat der Verkäufer die Möglichkeit Be better prepared for sales negotiations and to be able to argue better. The independent audit report makes him aware of the possible weaknesses from a buyer’s point of view.

The seller thus has the possibility to to consider in advance appropriate measures to optimise his business and to present these accordingly during the sales negotiations.

A VDD is also particularly useful if the seller intends to sell his company in an auction or bidding process. In this case, the vendor due diligence report can be the be made available to bidders as a basis for information.

This approach saves the potential buyers the financial effort and human resources, as they do not have to carry out due diligence themselves before they have even bid on the company.

Conclusion

Vendor due diligence can make sense for the seller and provides him with some advantages. At the same time, this type of approach is also cost-intensive and does not guarantee a sale at the price desired by the seller.

The VDD evaluates the company neutrally and reveals both positive aspects and grievances. This gives the seller the opportunity to react at an early stage and strengthens him in the sales negotiations..

Gerade für Verkäufer, die Zeit sparen möchten, ein Bieterverfahren planen und vorab im Detail noch besser die Schwächen ihrer Unternehmung von Dritten aufgezeigt bekommen möchten, könnten mit der Vendor Due Diligence einen guten Weg beschreiten.

If the seller commissions a VDD and hands out the fact book to the potential buyers, this also creates confidence on the buyer side and also saves the buyer the cost and effort of first carrying out an inspection himself.

This Ultimately accelerates the transaction process and reinforces a positive outcome.